Fed Chairman Powell Comments

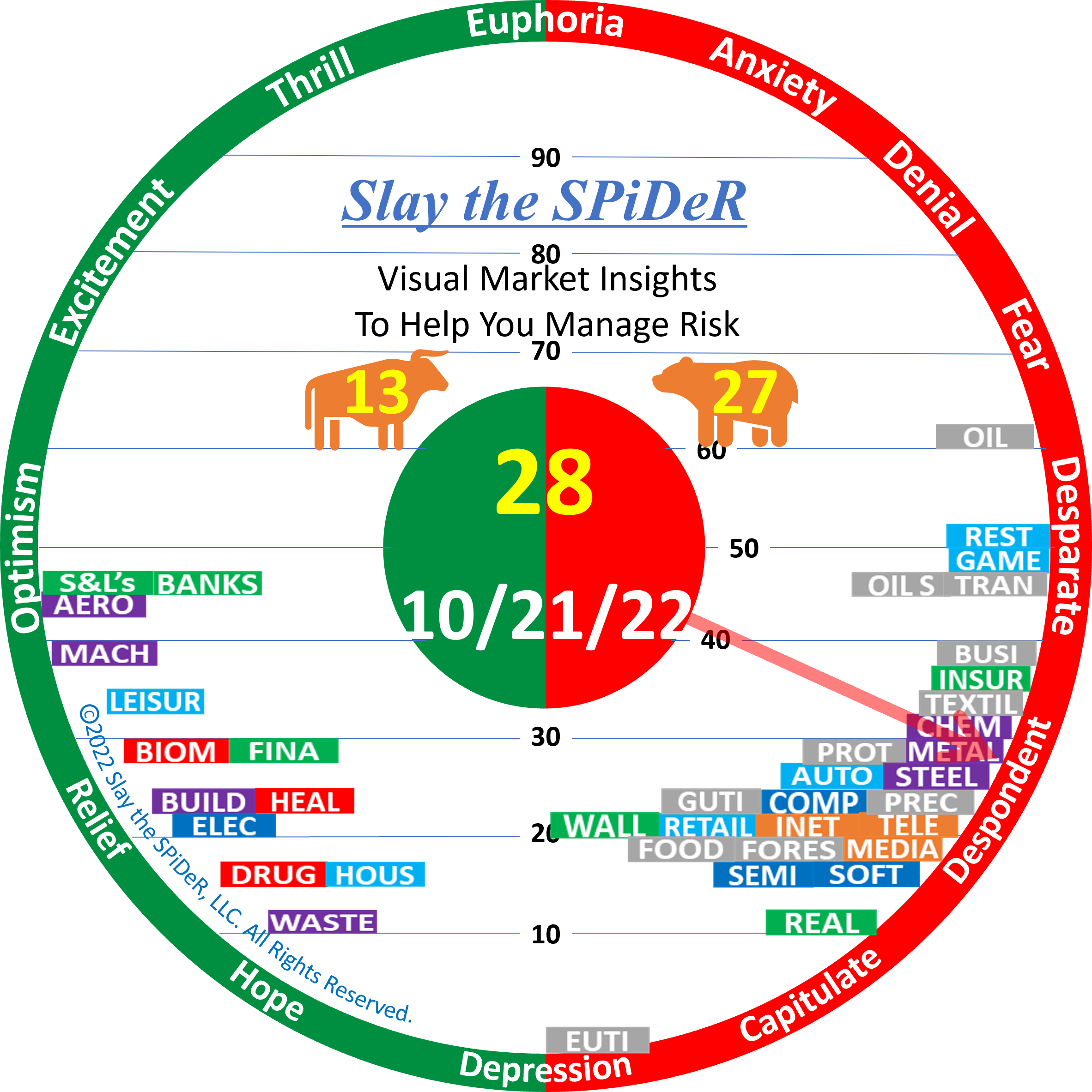

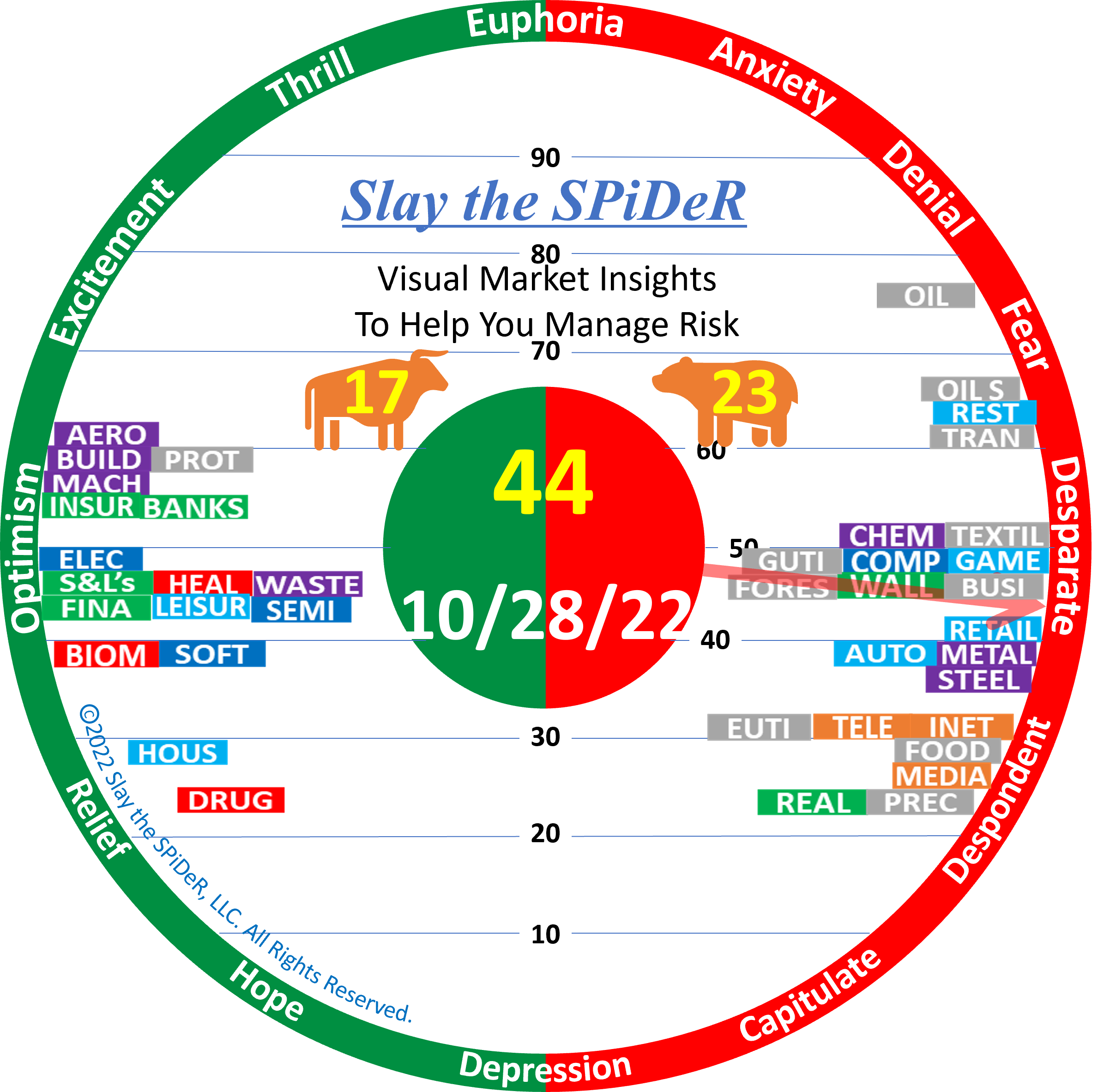

Slay The SPiDeR Newsletter 2022-10-28

Fed Rate Hikes

The Fed hiked rates 0.75% at the November 2 meeting. Afterward, Fed Chairman Powell had a Q&A where he said a few things which clearly outlined what the intent of the Fed is going forward.

First, he stated that the Fed has 2 mandates from Congress. They are low unemployment and low inflation rates. Those were the mandates created by Congress when the Fed was created decades ago. It’s not going to change.

There are about twice as many job openings as there are unemployed workers. Powell is not worried or concerned at all about the employment mandate at this time. The Fed intends to focus on the inflation mandate until either the inflation rate is in their target area of 2% inflation, or layoffs and a recession affect the employment situation. That is the job of the Fed per the Congressional mandates.

There was much public discussion prior to the Fed meeting about the Fed possibly pausing the rate hikes to allow more time for the rate hikes to take effect. Powell stated there was zero discussion of such a pause at the Fed meetings. Nor would there be unless the current circumstances changed significantly regarding the effects the hikes were causing, or the employment situation changed negatively.

In fact, Powell stated that the Fed has not seen any substantial effects of the hikes slowing inflation, despite the 5 rate hikes since March, including the past three 0.75% rate hikes in June, July, and September. He attributed this to the fact that savings are higher than they have ever been, and Americans are continuing to spend. The hikes have not yet significantly slowed demand. Slowing demand is the purpose and intent of the rate hikes. That is how inflation gets curbed.

My translation of Powell’s comments are that we will get another 0.75% hike in December, and beyond, unless there is clear evidence it is already working.

I always watch the Q&A sessions after the Fed meetings. The comments by Powell after the September meeting and the November meeting have me absolutely convinced that Powell and the Fed is not going to be letting up on the rate hikes until they are producing the disired results of reducing inflation.

It’s certainly not good news for the real estate and related businesses. Sales are already down 50% from a year ago. Mortgage brokers and bankers are beginning to get laid off as there is unsufficient business to support the reduced workloads. This will filter down to real estate brokerages, realtors, title companies, bankers, etc.

The rate hikes are also going to effect how long people stay in their current homes. Most people who have owned homes for more than a year or two have very low mortgage rates on their homes. If they sold and moved into a new or existing home, their mortgage rates would go from roughly 3% to over 7%. Unless someone has to move for a promotion or a new job, they are going to be very reluctant to double their house payment (at a minimum) for a comparable home.

In fact, the current higher rates will force many to stay in their current homes for many years to come. This will directly affect how many existing homes come onto the resale markets for decades, thus creating more shortages and hence higher prices.

Higher prices + higher mortgage rates are going to last for many years.

Portfolio Recommendations

I’ve recently looked at performance data in several sectors to see which stocks are doing well in the rallies, and doing lousy in the down markets.

It’s changing rather dramatically, more so than normal. There clearly is a move away from growth stocks, especially those companies whose revenues are growing but who are not profitable companies. Investors are clearly moving into companies that are both profitable and have dividend growth.

I am also seeing more erosion in the top tier companies, the 173 companies that comprise a combination of the S&P 100 and the Nasdaq 100. In a way, that is good news because it means we are in fact getting closer to a market bottom. Those companies are always the last to be hurt.

Of the 5 American companies who had market caps over $1 Trillion, now there are 3. Amazon and Tesla no longer have trillion $ market caps. I think Alphabet’s days with a market cap of $1 T are also limited because if the Republicans gain control of the House and Senate, section 230 laws are going to change.

Semiconductor companies are also going through a rough patch. I love investing in them, but clearly I only want to own profitable companies and clear market leaders such as Nvidia, AMD, ASML, TSMC, ADI, AVGO, etc. I expect them to also have a slow period, but ultimately they will survive, prosper, and buy up & comers like ON so that when the rebound does ultimately happen, they will again be market leaders. It will take some patience and some decisions. QCOM and INTC are not looking good at the moment.

The same is true in software. Buy MSFT, CRM, ADBE, ADSK. I love the revenue growth of DDOG and MDB, but they are not profitable yet. That represents risk in this environment.

In the Industrials, I am seeing more strength in companies like CAT, DE, and BA. Boeing in particular is looking better, finally. It could be a huge 2023 winner. DOV and DHR are looking good too.

In the Financials, I still love owning Visa, PYPL, and JPM. PAYX and PAYC are also becoming attractive again at current prices. Not there yet at prices I want to pay for them, but getting closer.

I am still not considering being a buyer of Media/Communications and Consumer Discretionary stocks. They have been hammered, some deservedly so, and I think they will also suffer most at the end of this bear market.

I have not yet evaluated Healthcare, Energy, and Basic Materials.

Charts and Video’s

Video

The market began turning down late on Friday 10/28.

Be sure to vote.

Let’s Go Get the Money

or at least keep what we have.

JimB