The Fed Dilemma

The Fed has a problem.

The CPI inflation report for November was good news as the Year on Year CPI inflation came in lower than expected at 7.1%. There are many pundits out there saying that we likely might be past peak inflation, and concluding that the Fed should ease up on the rate hikes, even pause rate hikes entirely this meeting , to avoid sending the economy into a recession. It’s a valid concern and argument, especially from real estate related parties like realtors and mortgage bankers.

On the other hand, the Fed this year has repeatedly stated they don’t pay that much attention to the headline inflation of the CPI report because they prefer using the Core Consumer Inflation report. It usually comes in much lower than the CPI inflation number. In November, this Core inflation report came in substantially above expectations, which is the opposite of the primary CPI result.

The dilemma for the Fed is whether or not to stick with their preferred indicator. They could and would lose considerable credibility and trust if they throw out the Core Indicator results and switch to the higher CPI. I just don’t see Powell agreeing to do that.

The markets were giddy Tuesday on the CPI report. The DJIA opened 265 points higher than the previous close and was up 707 within the first 15 minutes,. Then it gave up most of the gains and closed just 104 points higher for the day and lower than the opening price.

I think that happened because traders realized that the Fed has met its mandate of full employment and is still behind the curve on their mandate to control inflation.

The Fed is well aware that the reason the November inflation was better than expected was the sudden drop in energy prices due to the Chinese lockdowns and crude oil purchase cancellations. That caused a glut of oil in the markets, and the Crude Oil price drops, thus reducing inflation . Crude will go back up in price when the Chinese lockdowns end because the Saudi’s cut production by over 2.5 million barrels per day. I expect that to happen in late January after the Chinese New Year break.

Thus, the Fed really knows the current CPIinflation dip is temporary, or transitory, as they claimed was the case for inflation last year. We probably won’t hear that term used this time around.

If the Fed doesn’t stick to using their preferrred Core inflation, they will lose my confidence and trust.

Charts and Video

Chart

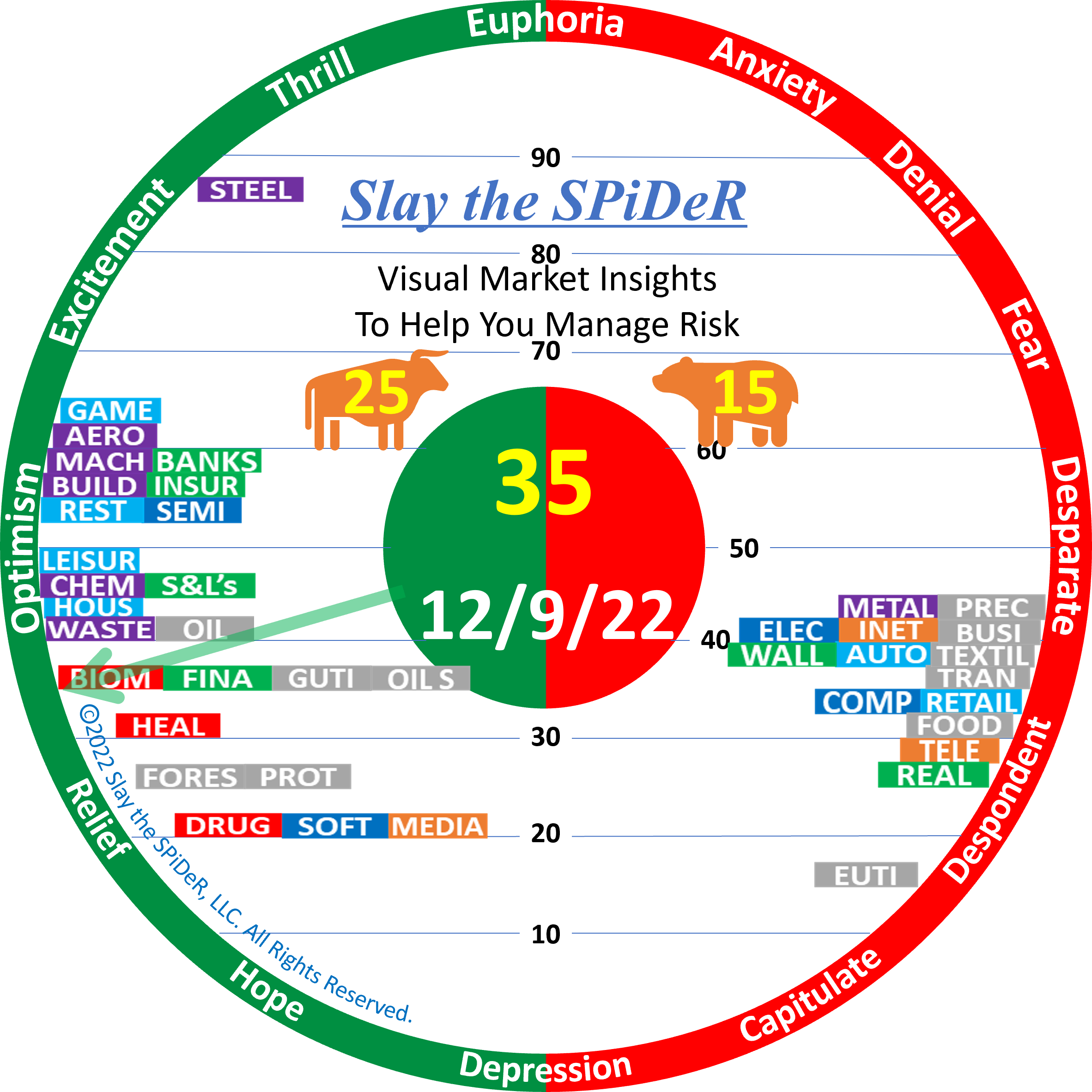

Strength in the market is still in the Industrial and Financials stocks.

Video

We still have a double top in place after the rally on Tuesday morning. and we have room on the charts for a 2% rally before it fizzles.

Let’s Go Get the Money

or at least keep what we have.

JimB