The Final Leg Down?

Slay the SPiDeR Newsletter 2022 12 02

The final leg down in this market may have commenced this past week.

I believe this is a very high probability because we just completed a 4th double top in the S&P 500 in 2022. The first 3 all resulted in double digit downturns within 8-13 days of trading after the double top. The details are in this weeks video.

The primary reason I think this may be the final down leg is because the blue chip stocks, like Apple, Microsoft, Amazon, Tesla, Alphabet, etc. are declining faster than the overall markets since the double top on Nov. 25th. Those stocks are always the last to experience the worst of the bear markets because they have the financial strength to be the last resort for safety (within the equity securities community.)

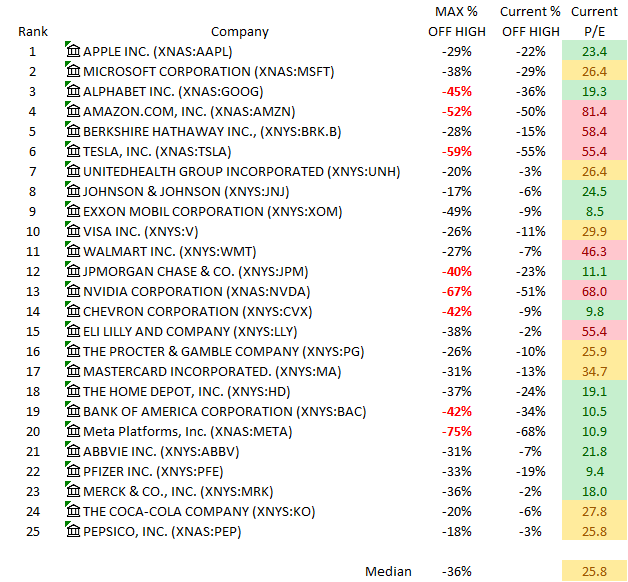

The 50 largest companies by market cap are listed below. They still have rather high P/E’s and need to come down substantially before we hit a bottom. Why? Interest rates are rising, Inflation is rising, 2023 earnings expected to be 11% lower than 2022. You cannot have high P/E’s with those 3 criteria happening.

Since the Nov. 25th double top, the S&P 500 has already lost about 4%.

Keep this in mind however. We are approaching year end. There are still 4 weeks for investors and institutions to harvest tax losses. There are plenty of opportunities because the bear market began January 4th, and a very high percentage of stocks have lost money this year. I think a lot of tax loss harvesting occurred in early October, and the subsequent 15% market rally has provided new buys, and many did not expect this year-end down leg. So there will be more opportunities for tax loss harvesting this month.

We also have a CPI and PPI reports for November coming out next week. The CPI will come out just as the Fed is meeting for the last time in 2022, and an expected rate hike on next week Wednesday (the 14th.) I am expecting the CPI to show another decrease in the inflation rate, and perhaps quite substantial. The reason is that crude prices have dropped sharply due to the worldwide glut of oil. That was caused by China shutting down again due to covid outbreaks. China cancelled orders for huge amounts of oil from the Middle East because China was shutting down industrial production in many manufacturing centers around China.

As a result, Saudi Arabia reduced production by another 500,000 barrels/day. And that was after a November reduction of 2 million barrels/day from the approximately 10 mllion barrels/day level of production just 5 weeks ago. They are now producing 7.1 million barrels/day.

Charts and Video

Chart

Video

What can we expect going forward?

The Fed has 2 mandates.

The full employment mandate is clearly being met with 1.3 job openings for every unemployed person. Wage pressures are also rising according to the Bureau of Labor Statistics.

The Fed inflation mandate is not being met. Since those are the 2 mandates to the Fed from Congress, the Fed is going to err in favor of taking action in regard to the mandate not being met by the Fed. That would be actions of fighting inflation… rate hikes. The Fed is certainly not going to pause rate hikes yet since they are still seeing only 1 mandate not being met. It’s just a debate about a 50 or 75 basis point hike in my opinion.

I think we will see a significantly lower level in the S&P before the CPI report next week. After the good news of the CPI report, a sharp rally up prior to the Fed meeting. Then, the surprise will be in the Fed statements after the rate hike announcement. Finally, year-end tax-loss harvesting.

In brief, a very volatile market over the rest of the month.

Layoffs, particularly in tech, retail and banking, are a worry for this holiday shopping season. Amazon laying off over 10,000 5 weeks before Christmas is a very big concern. The banks are laying off in the mortgage department and investment banks are trimming deal staffing as well. Some banks report seeing consumers spending a bit less this holiday season, but Retail still seems in decent shape with low unemployment nationally.

If I recall correctly from the bout of inflation in 1980, consumers were loathe to cut back holiday spending during the worst of that period. I think we are seeing that again.

Let’s Go Get the Money

or at least keep what we have.

JimB